Good morning,

Washington’s political stalemate concluded yesterday as President Donald Trump signed legislation to end a record-breaking 43-day government shutdown – eclipsing the 35-day impasse in 2018 to become the longest in US history.

Back to Work as Trump Puts Pen to Paper

Finally, the US government will be opening its doors, as President Donald Trump signed the legislation to end the shutdown. While things will eventually return to some semblance of normality, the reality is rather more complicated, and the implications for markets and economic data are only just beginning to unfold.

While workers return to their desks today, it will likely take some time to be fully operational. It is now all about the economic data and what the Fed does in December. With the central bank essentially flying blind for weeks, the Fed remains between a rock and a hard place for next month’s meeting. Notably, the White House observed that October prints for and jobs are unlikely to see the light of day!

In terms of Fed rate-cut expectations, we have seen a moderate hawkish repricing, with 14 bps of easing implied (a 55% chance of a ), and a total of 80 bps worth of cuts by the end of 2026.

Market Snapshot

In the markets, as you would expect, US stocks caught a bid. Cash markets saw the rally more than 300 points to notch a fresh all-time high of 48,254.82, or 0.7%. It was a quiet session for the , which largely flatlined, with the actually shedding around 0.3%. However, US equity index futures are moderately on the front foot this morning.

Meanwhile, precious metals rallied. extended gains for a fourth consecutive session, adding 1.7% and is fast closing in on the all-time high of US$4,381. also rallied 4.0% and is on the doorstep of challenging record highs of US$54.45. , however, took a sizeable hit – WTI Oil down more than 4.0% – after OPEC noted supply is expected to begin outpacing demand.

In the FX space, the ended the session largely unchanged, albeit considerably off its best levels. Ultimately, although the JPY was sold into ( up 0.4%), it was quiet across currencies.

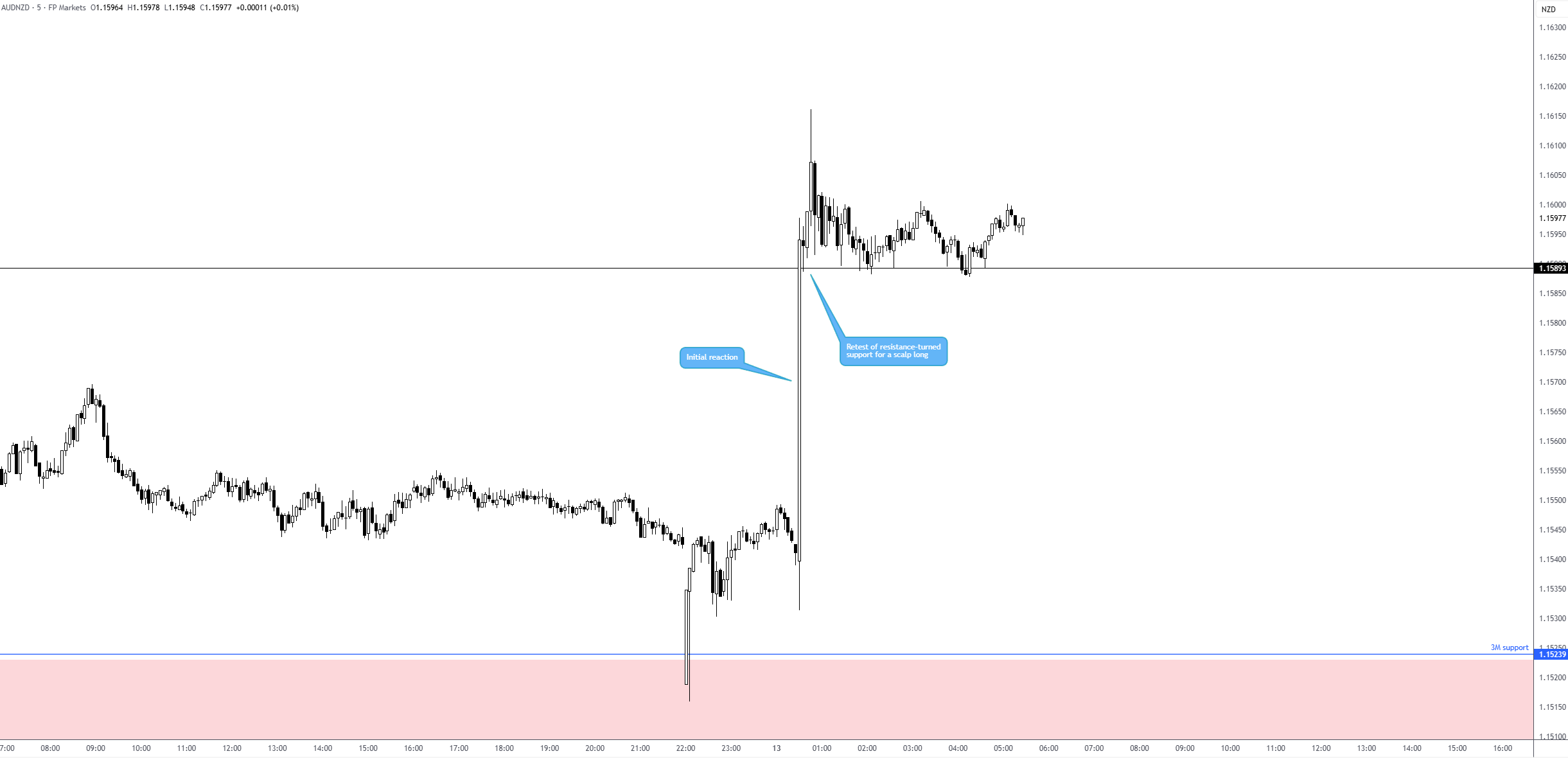

I do want to shine some of the spotlight on the , nevertheless, which remains higher versus G10 peers following an upside surprise in the October Aussie jobs report. Employment surged by 42,200, comfortably beating the 20,000 consensus, while unemployment came in at 4.3%, down from the expected 4.5% in September.

The cross (see below) offered a short-term scalping opportunity to enter long out of the event on the M5 chart; you may recall that I noted this market to watch closely in the event data printed at max/min estimates, which it did.

Source: TradingView

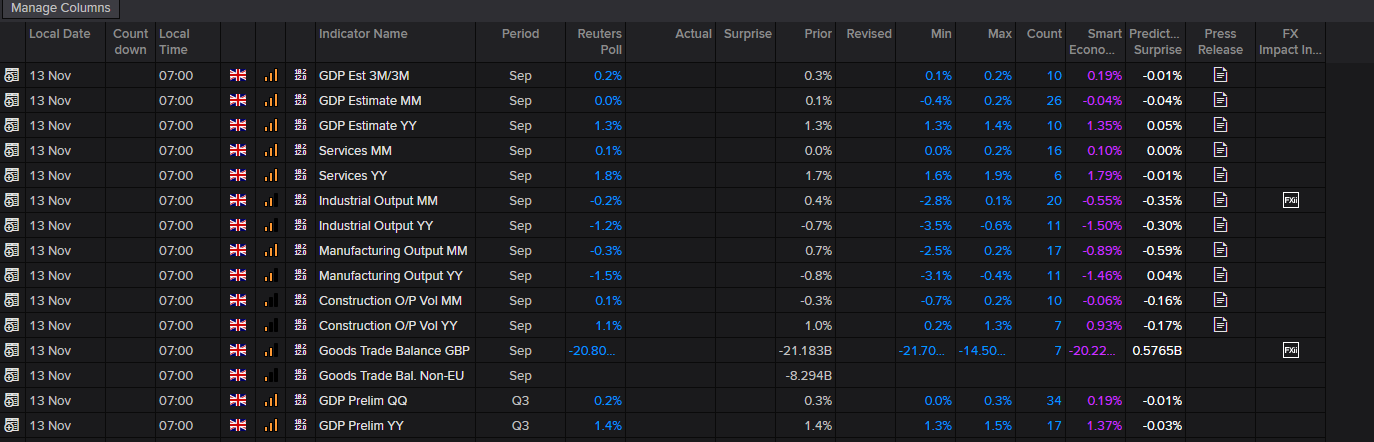

September UK GDP Ahead

Closer to home, in about an hour (7:00 am GMT), the September data will land. With inflation still sticky and growth anaemic, and softer-than-expected jobs numbers echoing a stagflation landscape, the BoE faces its own delicate balancing act. This follows a tight 5-4 MPC vote split to hold the bank rate unchanged at 4.00% last week, with markets pricing in 20 bps of easing for December’s meeting (82% probability).

As per the LSEG economic calendar below, MM data is expected to stagnate, down from 0.1% in August. The Q3 data is expected to have grown by 0.2%, slower than Q2’s 0.3%. I will leave you with what I noted yesterday, as my outlook remains unchanged:

‘Given the lack of volatility from the – which surprised me, as it was a textbook shorting opportunity – I feel traders will need to see more pronounced deviations to get involved, with at least the maximum or minimum estimates reached. Furthermore, given where the UK economy is right now and the upcoming Budget, a miss in the data could offer more bang for your buck for GBP shorts (primarily looking at EUR/GBP longs or GBP/NZD short plays). This may also prompt money markets to fully price in a BoE rate cut next month’.

Source: LSEG data