There’s not much on this week’s economic calendar. The only big event was supposed to occur on Wednesday, July 9. That would have been 90 days after President Donald Trump postponed his April 2 reciprocal tariffs on America’s trading partners on April 9 for 90 days. Today, that deadline was postponed again, to August 1.

This morning, Treasury Secretary Scott Bessent said in an interview on CNN’s “State of the Union” that a country’s tariffs will go back to April 2 levels on August 1 if there is no progress on signing a deal with the US. Bessent also said, “I would expect to see several big announcements over the next couple of days.”

In recent weeks, many investors bought stocks as they stopped panicking over Trump’s trade war. That’s because corporate earnings and the economy continued to confound the pessimists. The surged 26% since the correction low on April 8. The economy is still showing signs of resilience, most recently with the 147,000 increase in June payrolls and unemployment dropping to 4.1%.

Here’s a look at data reports coming out this week, which collectively are likely to reassure Federal Reserve officials that their wait-and-see approach to is the right one:

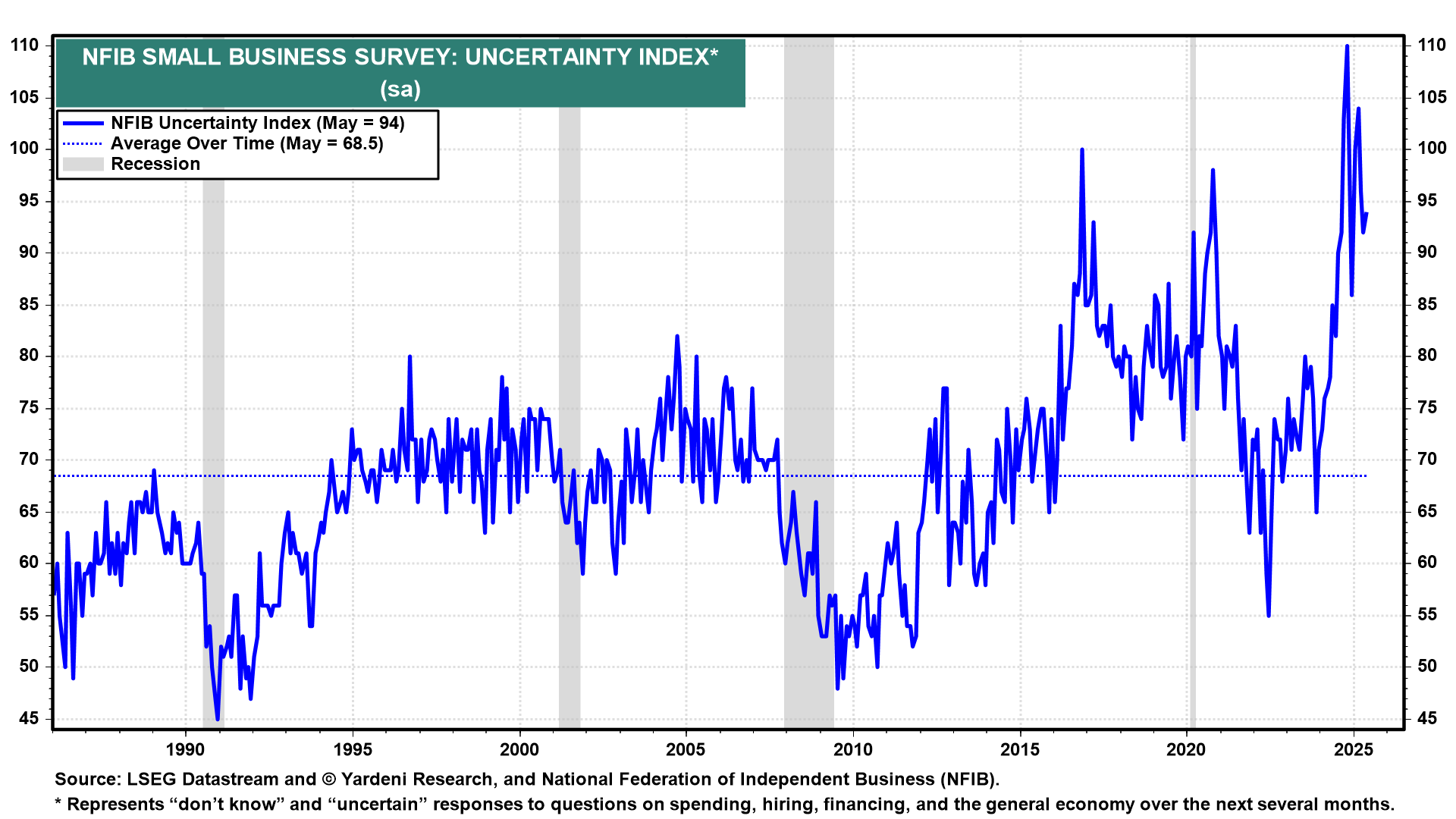

(1) . The results of the National Federation of Independent Business June survey of small business owners (Tue) are likely to show some improvement. The Optimism Index should rise from 98.7 in May closer to 100.0, reflecting a steadier-than-expected economy as confirmed by record stock prices.

The Uncertainty Index should edge down for the same reason despite lingering uncertainties about Trump’s tariff policies (chart). We will be focusing on the survey’s timely labor market indicators for confirmation that the jobs market remains resilient.

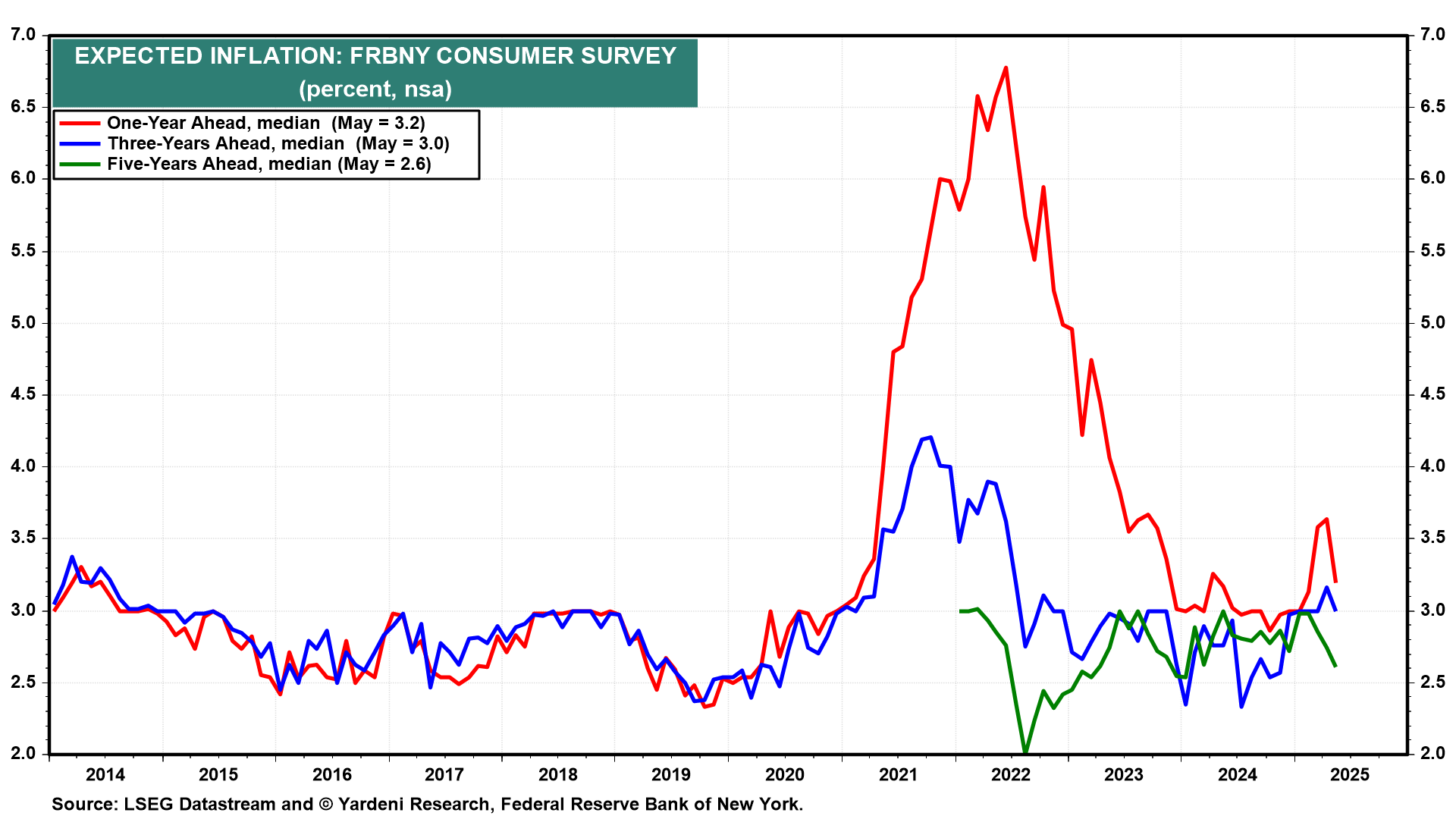

(2) Inflation expectations. The New York Fed’s June survey (Tue) should confirm that May’s drop was no fluke (chart). That would confirm the Cleveland Fed’s inflation Nowcasting model showing m/m increases of only 0.25% in June and 0.07% in July!

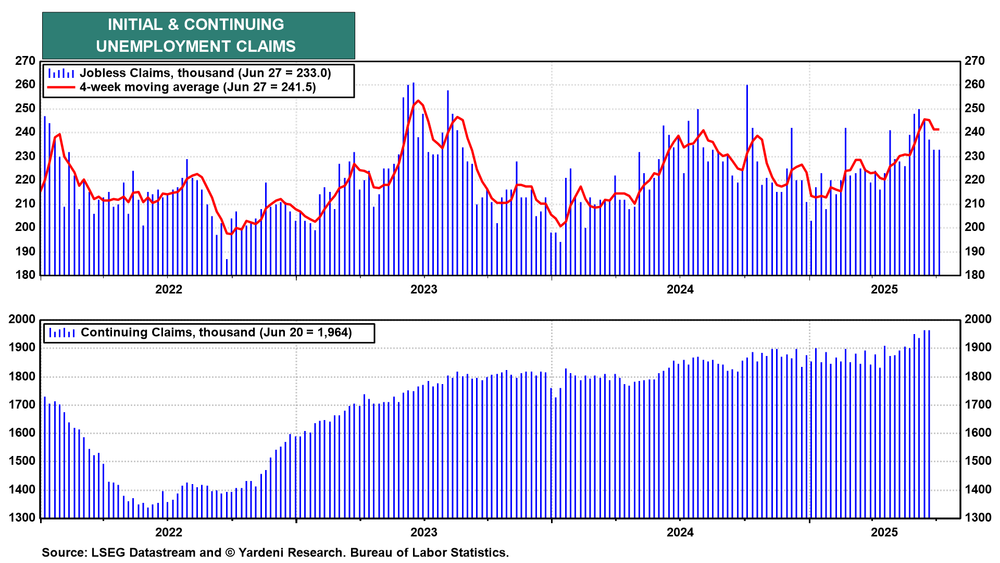

(3) Unemployment claims. We expect (Thu) to remain within the recent low range, continuing to prove wrong recent worries about layoffs (chart). It’s possible that will continue to suggest that the duration of unemployment is increasing, though that was not confirmed by June’s decline in the unemployment rate to 4.1% from 4.2% in May.

(4) Federal budget. US federal deficit figures for June (Fri) take on even greater weight considering the passage of Trump’s Big Beautiful Bill. Now that he signed it into law on July 4, let’s see how the bond market reacts to it. The yield rose to 4.35% on Thursday following the better-than-expected June employment report. We are still forecasting that the yield will range between 4.25% and 4.75% through the end of this year.