Confidence in the US dollar remains low in global markets. The , hovering around 97, is very close to its lowest level in the past three years. Domestic political uncertainties and signals of possible monetary policy intervention have played a key role in this decline. In particular, President Donald Trump’s increasing pressure on the , and his open desire to replace Jerome Powell with a more dovish chair, have raised concerns in the markets about the Fed’s independence.

Political Pressure on the Fed: Monetary Policy Independence Back on the Agenda

Trump’s remarks on Fox News regarding —stating that the Fed should cut its policy rate to 1–2%—and his explicit wish to replace Powell have increased speculation about a “politically motivated monetary policy.” Reports last week that Trump may soon announce Powell’s successor have added to fears that he could speed up the process. This has brought the Fed’s independence back into question and is seen as a factor contributing to the medium-term structural weakening of the dollar.

Market pricing for the Fed’s next moves is also being shaped by this backdrop. Fed Chair ’s remarks in Congress, suggesting a rate cut was on the table if inflation does not rise significantly during the summer, were interpreted by markets as a clear dovish signal. According to market expectations, the probability of a 25 basis point rate cut in September has risen to 91.5%. While some analysts believe the market is pricing in too much, the underlying pressures on the dollar remain intact.

Trump’s Giant Budget Deficit Plan Also Challenges the Dollar

Another major factor undermining the dollar’s strength is concern over the Trump administration’s economic policies. The Congressional Budget Office (CBO) estimates that Trump’s $4.2 trillion tax cut and spending package—recently passed by the Senate—could widen the budget deficit by $3.3 trillion between 2025 and 2034. This could strain the U.S. debt outlook and weigh on the dollar’s long-term status as a reserve currency.

Trump’s aggressive rhetoric toward Iran and renewed trade tensions with Canada over the digital services tax are also dampening global risk appetite and reducing demand for the dollar. Although Canada has since reversed the tax and resumed talks with the U.S. and China, the threat of new tariffs after July 9 is reintroducing market anxiety.

On the macroeconomic side, May data in the U.S. came in above expectations at 2.7% year-over-year. This triggered a rise in bond yields but still indicated that inflation expectations remain anchored. The decline in University of Michigan inflation expectations supports this view.

However, the key data point this week will be the report. If a labor market slowdown materializes as expected, the Fed may move more quickly toward a rate cut. If not, the optimism surrounding dovish expectations could fade. As such, data flow may lead to increased volatility this week.

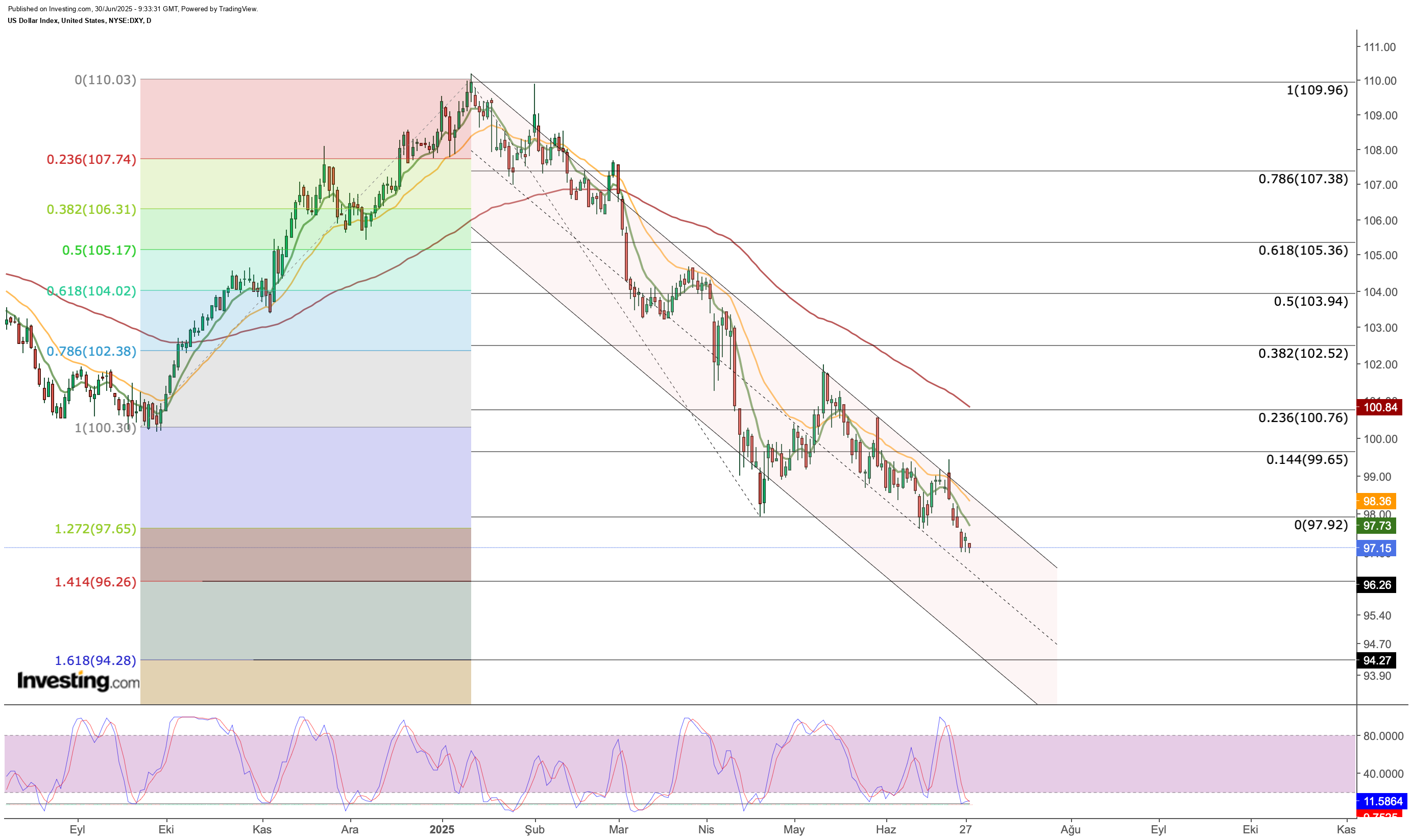

DXY Technical Outlook: Monitoring Critical Support Zone

The has recently fallen as low as 97, breaking below the support level at the Fib 1.272 extension—around 97.65—amid recent declines. This marks a move into the Fibonacci expansion zone from a technical standpoint.

The next support level in the DXY, which continues to move within a descending channel, stands at 96.25. If the intermediate support at the 97 level fails during the week’s volatility, we may see the index drop toward the 96 region. Conversely, if the 97 level holds, then 97.65 becomes the next immediate resistance. A break above that could trigger a move toward 98. Such a move would also represent an upward breakout from the descending channel. Should the DXY remain above 98 during the week on any rebound, this could establish a neutral outlook in the 98–100 band going forward. However, current developments suggest continued weakness in the dollar is more likely for now.

The next support level in the DXY, which continues to move within a descending channel, stands at 96.25. If the intermediate support at the 97 level fails during the week’s volatility, we may see the index drop toward the 96 region. Conversely, if the 97 level holds, then 97.65 becomes the next immediate resistance. A break above that could trigger a move toward 98. Such a move would also represent an upward breakout from the descending channel. Should the DXY remain above 98 during the week on any rebound, this could establish a neutral outlook in the 98–100 band going forward. However, current developments suggest continued weakness in the dollar is more likely for now.

Trump’s strong criticism of the Fed, aggressive fiscal policies that widen the budget deficit, and lingering trade uncertainties continue to weigh on the dollar in both structural and short-term contexts. Expectations for a rate cut by September remain high and will likely support further downward pressure on the DXY. In the coming period, employment data, inflation readings, and Trump’s statements following July 9 will remain key drivers of the . In conclusion, while the DXY remains under pressure in the short term, Fed policy and macroeconomic data will play a decisive role in determining its medium-term direction.

****

Be sure to check out InvestingPro to stay in sync with the market trend and what it means for your trading. Whether you’re a novice investor or a seasoned trader, leveraging InvestingPro can unlock a world of investment opportunities while minimizing risks amid the challenging market backdrop.

- ProPicks AI: AI-selected stock winners with proven track record.

- InvestingPro Fair Value: Instantly find out if a stock is underpriced or overvalued.

- Advanced Stock Screener: Search for the best stocks based on hundreds of selected filters, and criteria.

- Top Ideas: See what stocks billionaire investors such as Warren Buffett, Michael Burry, and George Soros are buying.

Disclaimer: This article is written for informational purposes only. It is not intended to encourage the purchase of assets in any way, nor does it constitute a solicitation, offer, recommendation or suggestion to invest. I would like to remind you that all assets are evaluated from multiple perspectives and are highly risky, so any investment decision and the associated risk belongs to the investor. We also do not provide any investment advisory services.

Disclaimer: This article is written for informational purposes only. It is not intended to encourage the purchase of assets in any way, nor does it constitute a solicitation, offer, recommendation or suggestion to invest. I would like to remind you that all assets are evaluated from multiple perspectives and are highly risky, so any investment decision and the associated risk belongs to the investor. We also do not provide any investment advisory services.