Using the US stock market as a guide suggests that business-cycle conditions remain strong in terms of the recovery since the current economic expansion began in May 2020.

The rebound in equities is still one of the sharpest since 1970. But the stock market is not the economy, as the saying goes, and that’s where the analysis turns complicated, as suggested by a review of key economic indicators.

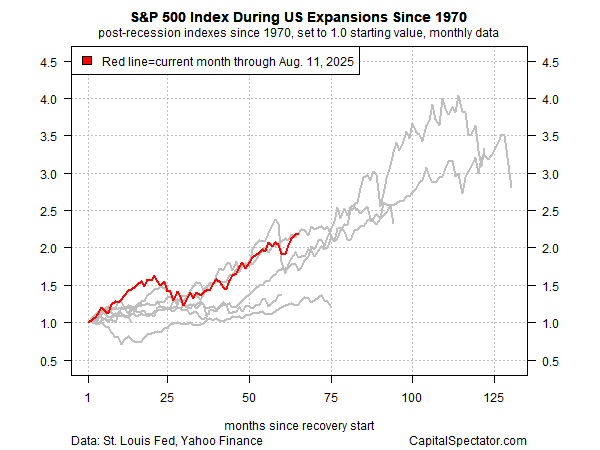

For perspective on how stocks differ from the real economy, let’s start with the . As the first chart shows, the market’s recovery since the last economic recession ended (based on NBER business cycle dates) remains relatively strong compared with rebounds following previous recessions.

An optimistic reading of this data also suggests that the current bull market potentially has a long way to go, assuming the recovery follows the path of the longest up cycles in the post-1970 period.

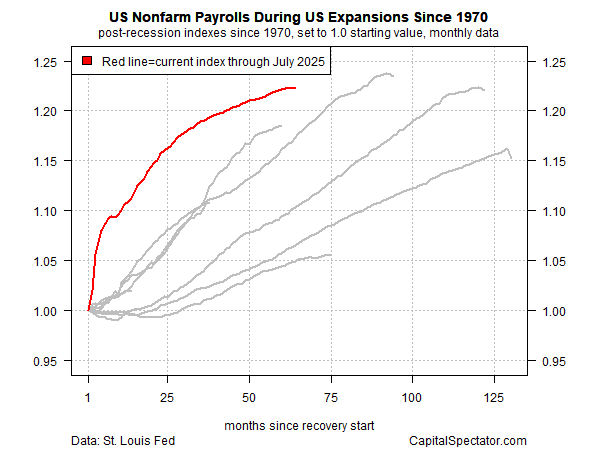

The analysis, however, becomes mixed as we review key US economic indicators. The recovery in fares the best for hard economic numbers and is still posting the strongest rebound since the recession ended for cycles since 1970. But the snapback following the pandemic shock was unusually strong and there are signs that labor market growth is now slowing.

The concern is that the stellar runup in job growth since the 2020 trough is unsustainable and therefore unusually vulnerable to the aging of the business cycle. For the moment, there’s data still reflects a strong trend in relative terms, but the next several months could be critical for deciding if the payrolls is susceptible to a reversal due to the unusual circumstances of the post-pandemic business cycle.

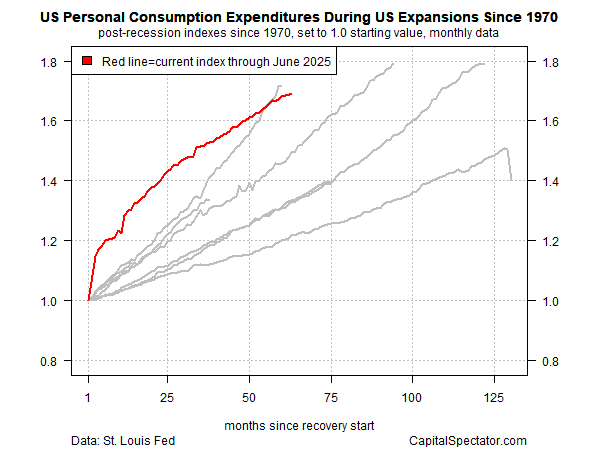

The recovery in since the end of the pandemic recession remains the second-strongest on record since 1970, but there are signs that it’s beginning to fade in relative terms. Here, too, the next several months could be decisive for analyzing the trend outlook and how/if tariffs will affect consumer spending.

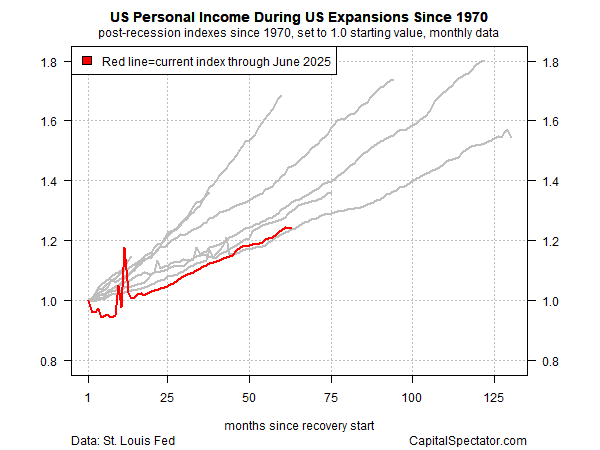

The recovery in , by contrast, has consistently been weak in relative terms. For several years following the end of the last recession, consumer income posted the slowest rebound since 1970. The pace has picked up slightly, but the recovery remains tepid – a key risk factor for the economy if payrolls weaken further in the months ahead.

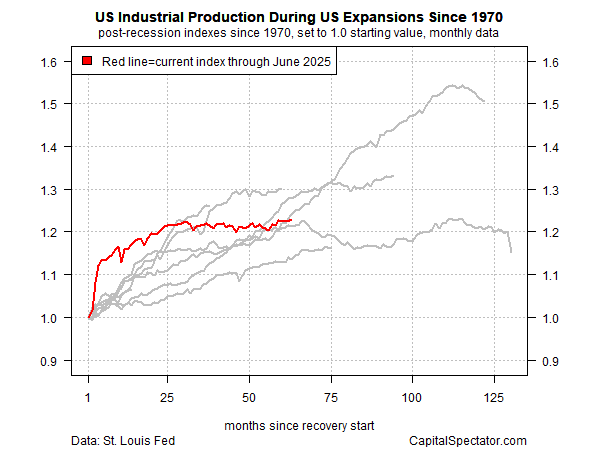

Finally, ’s strong rebound since the pandemic faded a couple of years ago and continues to flatline. The implication: to the extent that the economic expansion requires support from industrial activity, the outlook remains cautious on this front.