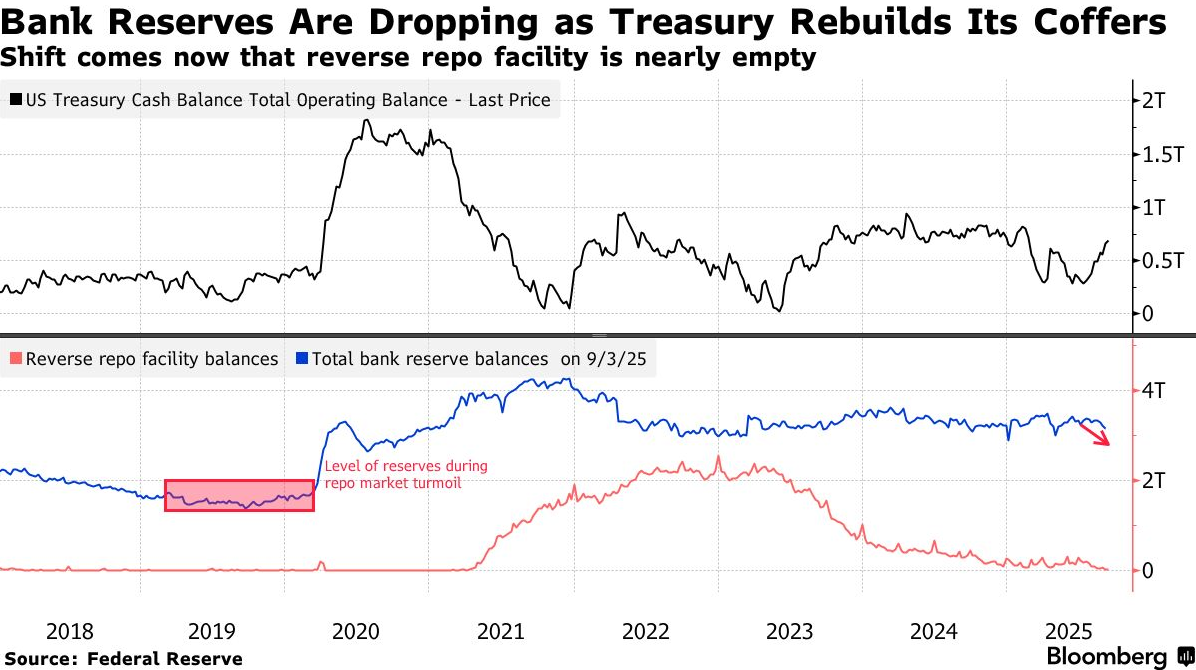

After years of abundant liquidity, U.S. overnight funding markets are beginning to show signs of strain. Interest rates on overnight repo agreements have climbed steadily this month as the Treasury rebuilds its cash balance and the Fed continues quantitative tightening. Usage of the Fed’s overnight reverse repo (RRP) facility, a key gauge of excess liquidity, has dropped to a four-year low. The result has been a widening spread between repo and fed funds rates, indicating that money market conditions are tightening. As recently noted by Bloomberg,

Since the beginning of September, the gap between repo and the federal funds rate has grown to about 11.5 basis points on average, the widest level since the end of April. That spread was in single digits in July and August as market participants were able to digest supply by shifting allocations to T-bills from repo.

The chart below clearly illustrates the impact of this year’s Treasury refunding on bank liquidity. With the overnight RRP facility now nearly empty, traders fear further stress as corporate tax payments and Treasury auctions settle this week, potentially draining more liquidity. Further, the Treasury is slated to ramp up bill issuance again in October. Standing repo facilities introduced after the 2019 “repocalypse” should prevent a disorderly spike in overnight repo rates. However, the risk of higher funding costs may be here to stay unless the Fed puts an end to QT.

The Week Ahead

It’s a heavy week for economic data and the Fed. Today kicks off with the survey, which is expected to remain in expansion after last month’s strong rebound.

Tomorrow, all eyes turn to , with expectations calling for another solid gain in the headline figure after July’s increase. Economists expect the retail sales control group, which feeds the calculation, to soften slightly from July’s 0.5% increase. The control group surprised to the upside in each of the last two reports. Thus, another positive surprise for August isn’t out of the question.

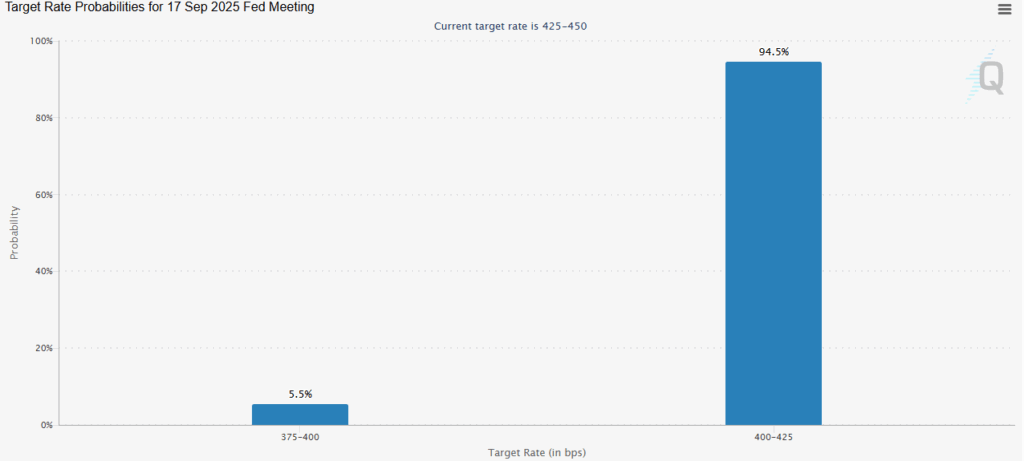

Wednesday brings the most important event of the week: the FOMC and an updated summary of economic projections (SEP). As shown below, markets are pricing in a 25-basis-point cut with near certainty. Thus, the press conference will be closely parsed for clues on whether the Fed leans toward further rate cuts in the months ahead. Housing starts and building permits data also hit before the market opens.

Thursday closes this week’s economic data with . Markets will be watching closely to see if last week’s sudden jump above 260k was noise or a signal of further softening in the labor market. The will also be released, providing another look into regional manufacturing conditions.

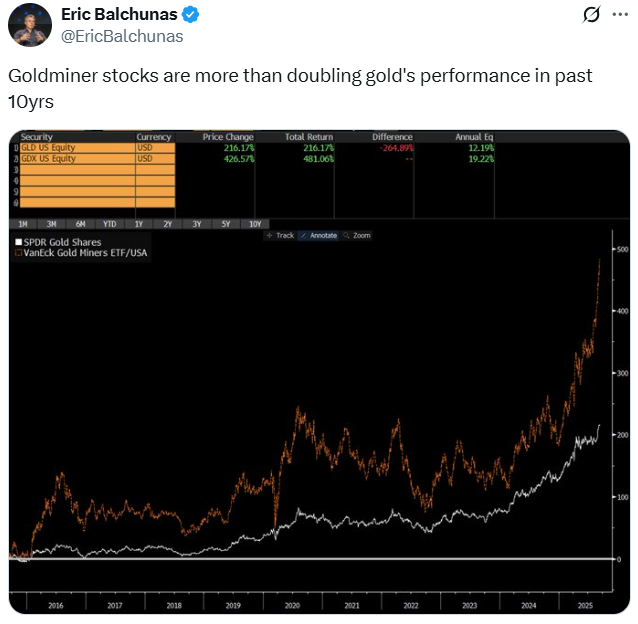

Tweet of the Day