European Session Recap

European markets began the day on the back foot as market participants digested a proposed tax-cut bill that threatened to enlarge the US deficit.

Opposition to President Trump’s tax plans and the growing deficit is impacting the bond market, with Treasury prices dropping on Wednesday and dragging down other U.S. assets. The concern is that the tax bill could add trillions to the already large budget deficit in the coming years, especially as global interest in U.S. assets declines.

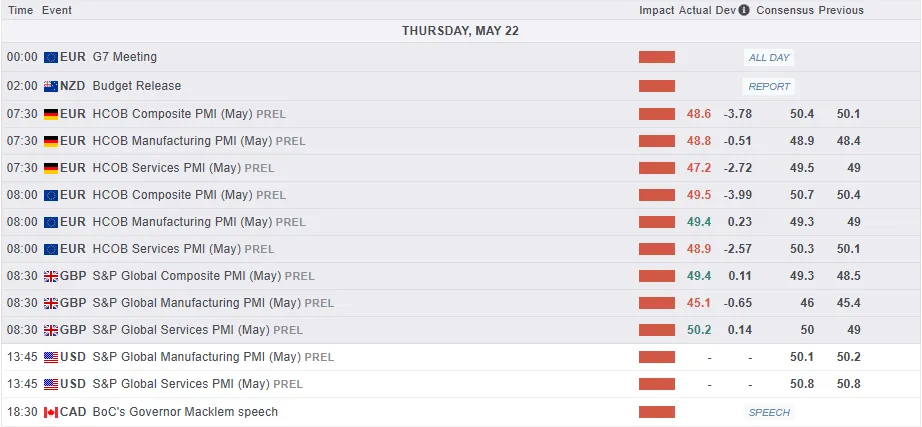

European Data Mixed as German Ifo Beats But PMI Disappoints

European data released this morning revealed a mixed picture. In Germany business sentiment has improved which is a positive sign in light of sentiment data out of the US last week.

German businesses are cautiously optimistic despite US tariff concerns. They’re focusing on potential positives from the new German government rather than trade uncertainties. The rose to 87.3 in May from 86.9 in April. While the current situation rating dipped slightly, future expectations jumped to 88.9, the highest in a year.

On the flip side, the dropped to 49.5 in May 2025, down from 50.4 in April, signaling the first decline in private sector activity this year. Both (48.9) and (49.4) saw declines, though factory contraction was the smallest in nearly three years.

fell as US-EU tariff risks and earlier stockpiling reduced demand. Despite this, job creation stayed steady due to existing order backlogs. Manufacturing costs decreased, but service costs rose sharply. Business confidence also hit its lowest point in 19 months.

The data has raised concerns that the Eurozone economy could be entering stagflation territory once more.

This has weighed on the this morning as it trades around 0.3% lower to the . The data has also kept the on the backfoot as it remains below the 24000 handle.

faced pressure this morning on rumors that OPEC + are discussing another 411k bpd output hike in July. This adds to market concerns around demand and could weigh Oil prices down moving forward.

The US Open

Heading into the US open and market participants may be cautious following Wednesday performance. All three major Wall Street indexes saw their biggest single-day drop in about 4 weeks as concerns around US debt continue to pile up.

In premarket trade today, Most big tech and growth stocks edged up in premarket trading, with Alphabet (NASDAQ:) (Google’s parent company) leading with a 1.3% gain.

Cryptocurrency-related stocks surged as hit a record high. Coinbase (NASDAQ:) rose 2.5%, MicroStrategy gained 1.4%, and crypto miner MARA Holdings jumped 4%.

Snowflake (NYSE:) soared 10.2% after the cloud company raised its product revenue forecast for 2026.

Given the US tax bill has passed the house sentiment may improve slightly ahead of US data. However, the concerns around the tax bill were largely down to a widening budget deficit and those still remain in play which could keep sentiment and thus risk assets in check.

Economic Data Releases

Looking ahead, the US session finally brings a bit of data today with , and data all scheduled for release.

Along with this we have at least two officials including New York Fed President slated to speak later in the day.

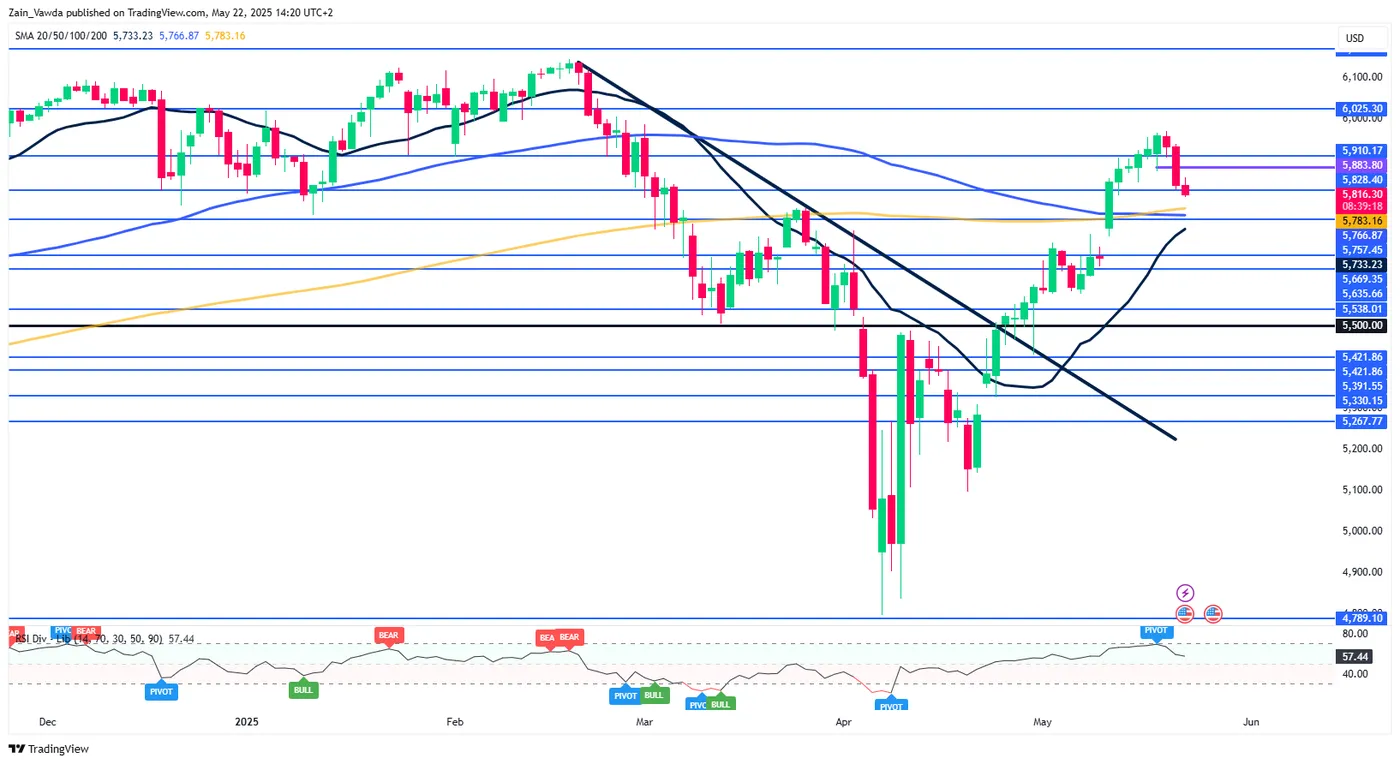

Chart of the Day – S&P 500

From a technical standpoint, the is approaching a key confluence level.

Having posted its biggest single-day drop in a month yesterday, a key confluence area rests just below the 5800 handle.

The levels between 5800-5736 plays host to the 20, 100 and 200-day MAs which could all be a source of support for the index. If this level holds, the probability of a fresh high is likely to improve.

On the daily timeframe, bulls remain firmly in control with a daily candle close below the 5580 swing low needed to invalidate the bullish structure.

Immediate support rests at 5800 before 5785 and 5736 come into focus.

If a move to the upside materializes, 5883 will be the first area to monitor before the 5910 and 5962 levels come into focus.

Source: TradingView.com