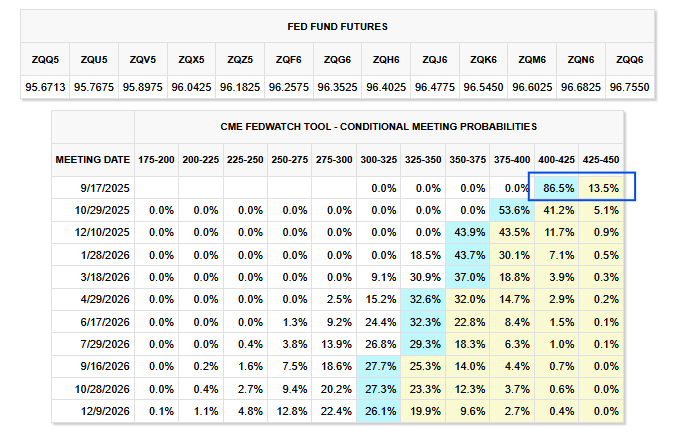

As we share below, the Fed Funds futures market is 86.5% confident the Fed will by 25 bps in September. However, they assign a zero percent chance that the Fed cuts by 50 bps. Powell’s trepidation to cut rates leaves traders unwilling to consider that anything more than 25bps is possible. We argue that despite the odds, a 50-bps rate cut is possible if today’s report is weak.

is expected to increase by 0.2% on a headline and basis. A 0.2% increase would bring the year-over-year rate to 2.7%, decently above the Fed’s 2.0% target. Even if CPI were to surprise with a 0% change, the year-over-year change would sit above the Fed’s target. Such is the market’s logic for not considering 50 bps. We think that a student shift lower in inflation, especially as tariffs are having a significant impact, coupled with the recent sharp negative revisions in employment data and new highs in continuing jobless claims, could be enough for the Fed to debate 50 bps.

Moreover, Stephen Miran may likely join the Fed by the September meeting, giving them at least three votes for a cut. Consider also that the two Fed members who voted for a rate cut at the last meeting may think they are already 25 bps behind the curve and want to vote for 50 bps to catch up. The political pressure is on Powell.

While he may not cave and vote for 50 bps in September, we think the market is underestimating the odds that a majority of members will. With zero odds, the market is vulnerable (up or down) for a sudden shift in the Fed’s rate projections.

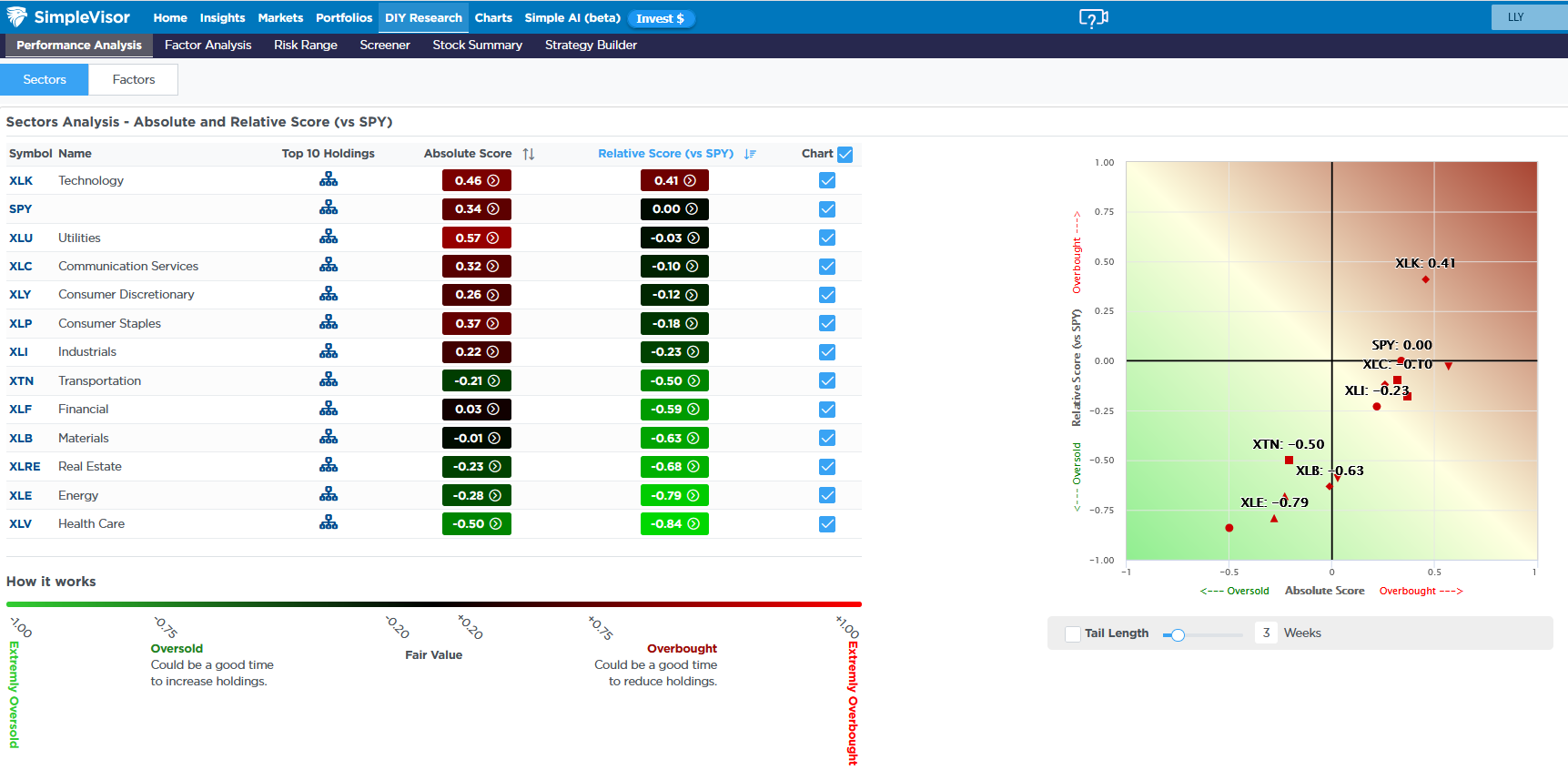

Apple And Technology Lead The Market Higher; Everything Else Lags

On a relative basis, the technology sector is the clear leader. As shown below, it is moderately overbought versus the market on a relative basis. Importantly, every other sector is near fair value or oversold versus the market. Apple (NASDAQ:), rising by over 12% last week versus the 2% for the S&P 500, helped push the technology sector up and to the right, indicating overbought conditions on a relative and absolute basis. As the graph shows, there is a clump of sectors at fair value, and another that are getting very oversold. Of the very oversold, healthcare weakened by sharp declines in Unitedhealth Group (NYSE:) and Eli Lilly (NYSE:) are now grossly oversold versus the market. The analysis argues that any shift in market tenor could see healthcare outperform and technology underperform.

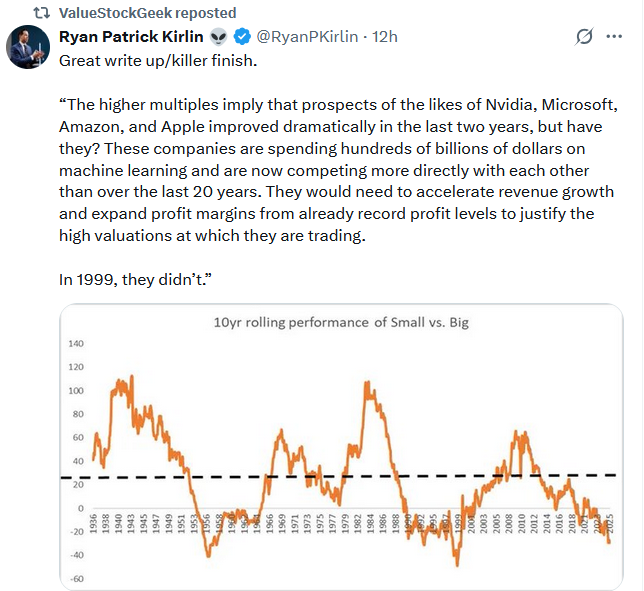

Tweet of the Day