- Middle East ceasefire and Fed shenanigans weigh on the dollar

- ISM PMIs and Nonfarm payrolls to impact Fed rate cut bets

- Eurozone inflation and ECB forum to be closely monitored by euro traders

- China PMIs, Japan’s Tankan Survey and Swiss CPI also in focus

Israel-Iran Ceasefire and Fed Independence Risks

The underperformed all its major peers this week, initially coming under pressure after US President Donald Trump announced a ceasefire between Israel and Iran. Although there were some violations of the ceasefire a few hours after the announcement, the accord was respected the last couple of days, allowing a risk-on market response. Equities on Wall Street rebounded strongly, collapsed as supply concerns eased, and the US dollar, which acted as the safe haven of choice for this conflict, pulled back.

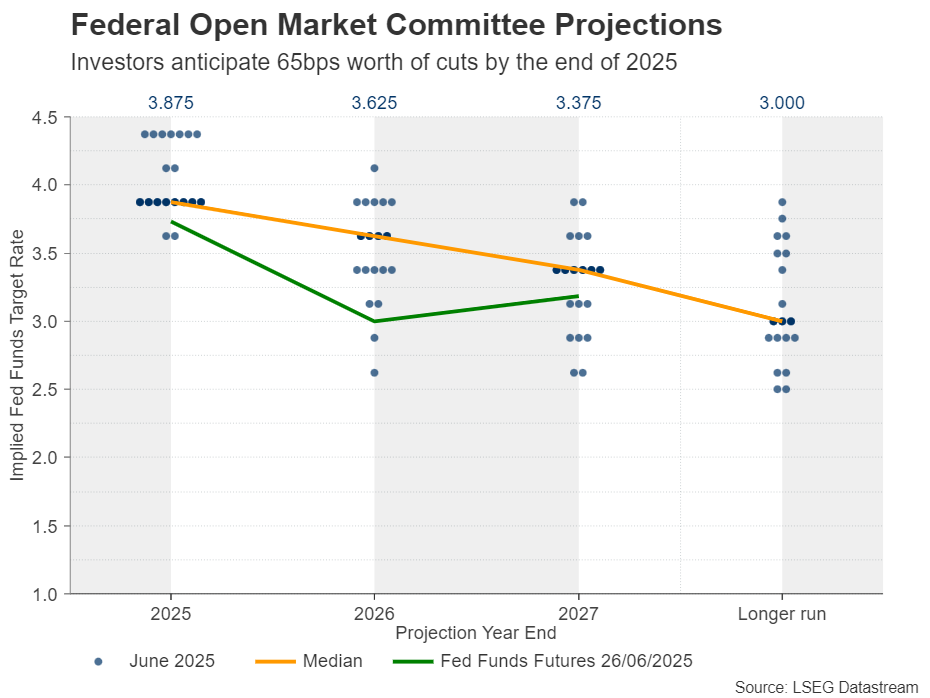

What may have also weighed on the US dollar were new attacks by President Trump on Fed Chair Powell about not lowering , with a Wall Street Journal report noting that the President is considering announcing Powell’s successor by September or October. This has raised concerns about the credibility and independence of the Federal Reserve and prompted investors to add to their rate cut bets.

According to Fed funds futures, market participants are now penciling in almost 65bps worth of rate cuts by the end of the year, which means that they agree with the two quarter-point reductions indicated by the Fed’s latest dot plot, but they are also seeing a more-than-50% chance for a third one. The first reduction is more than fully priced in for September, while the probability of acting as soon as in July has risen to 25%.

ISM PMIs and Nonfarm payrolls enter the spotlight

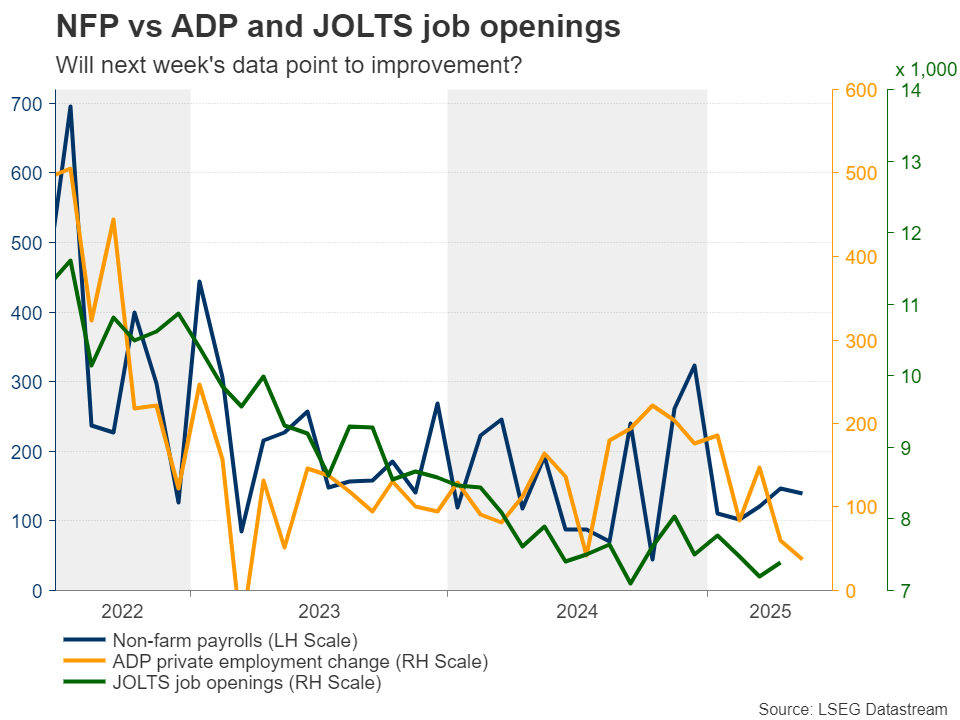

With all that in mind, as they try to better assess how the Fed may navigate monetary policy, investors are likely to pay extra attention to the ISM and PMIs for June, due out on Tuesday and Thursday, respectively, but the spotlight is likely to fall on the for the same month, scheduled to be released on Thursday, as on Friday, the US will be celebrating its Independence. The for May will come out on Tuesday and the private employment report for June on Wednesday.

This week, the preliminary S&P Global came in higher than expected. Although the pulled back somewhat to 52.8 from 53.0, it was decently higher than the 52.2 forecast. Price pressures rose sharply in both the and sectors, with the former sector reporting an especially steep increase due to tariffs.

What’s more, companies increased their employment at a rate not seen for just over a year, largely in response to higher workloads.

Should the ISM figures paint a similar picture, investors are likely to scale back their rate cut bets, especially if non-farm payrolls continue to indicate that the labor market is faring well. The US dollar is likely to rebound as the market becomes accustomed to the idea that the Fed could remain patient before resuming its rate-cut process.

However, with a couple of members already shifting to dovish and supporting a July cut, like Fed Governors Waller and Bowman, and the US President putting more pressure on Powell and his colleagues to lower borrowing cost, any recovery is likely to remain limited and short-lived. At this point, it is worth mentioning that Waller is rumoured to be among the candidates President Trump is considering for replacing Powell, which adds to concerns about the Fed’s independence.

Will the Eurozone CPI Data Corroborate ECB Rate Cut Bets?

Flying to Europe, with the dollar slipping and the market foreseeing only one quarter-point reduction in the ECB’s arsenal before this easing cycle ends, climbed to a nearly-four-year high.

Next week, euro traders will have to assess the Eurozone’s preliminary data for June, due out on Tuesday. At its latest gathering, the ECB decided to lower by 25bps, bringing the deposit rate to 2.0%, with President Lagarde noting at the press conference that the decision was not unanimous as one member did not support the decision to cut interest rates. She also said that they are in “good position” with the current rate path, with investors impterpreting the statement as increasing likelihood for a break in rate cuts. What’s more, citing four sources with direct knowledge of the discussion, Reuters noted that there was broad agreement at that meeting about taking the sidelines in July.

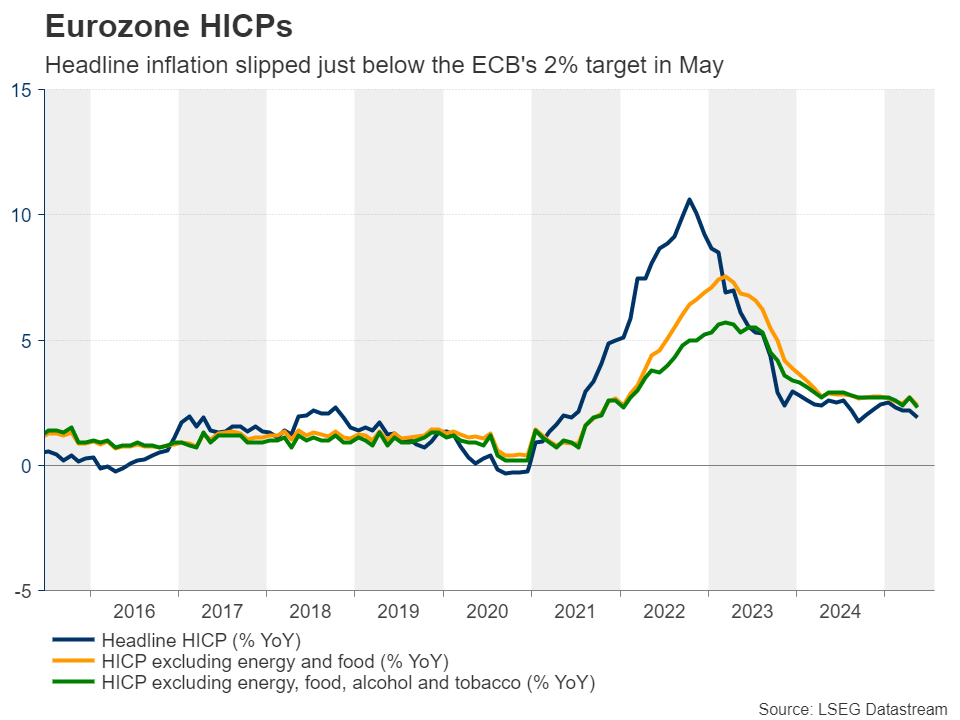

Since then, data revealed higher than expected growth for Q1, while for April accelerated to 2.3% y/y from 1.9%, instead of slowing to 1.4% as the forecast suggested. This corroborates the idea that the ECB could be a bit patient for now. However, the tumble in and the weaker-than expected for June keep the door wide open for at least one more rate cut, even if it is not delivered in July.

With President Lagarde noting again a few days ago that, at the current interest rate levels, they could navigate uncertain circumstances, and that they will follow a data-dependent approach, investors are unlikely to alter significantly their view, even if inflation accelerates somewhat. After all, the Euro area’s slipped to 1.9% y/y in May, a tick below the ECB’s objective of 2%.

Instead of expecting the next rate cut to be delivered in December, traders may just push that timing into the beginning of 2026, something that could support the euro somewhat. The preliminary of the Eurozone’s economic powerhouse, Germany, will be released on Monday, while the ECB forum on central banking begins the same day in Sintra, Portugal. ECB President Lagarde and other policymakers will hold speeches, while among the guests to participate in a policy panel is Fed Chair Jerome Powell.

China PMIs, Japan’s Tankan Survey and Swiss Deflation

Elsewhere, China’s official and PMIs for June, as well as Japan’s Tankan survey for Q1 are due to be released during the Asian sessions on Tuesday and Wednesday, respectively. Although the deadline of the 90-day tariff-delay Trump imposed to reach deals with the US’s main trading partners is fast approaching, China has a tentative accord that extends into mid-August, which allows time for a more concrete agreement.

The PMIs will reveal how the Chinese economy has been performing during this grace period and upbeat numbers could well benefit the currencies of and , which have close trading ties with the world’s second largest economy. As for the Tankan survey, with investors assigning a 50-50 chance of a BoJ rate hike at the end of this year or the start of the next, the outcome could tilt the scale accordingly.

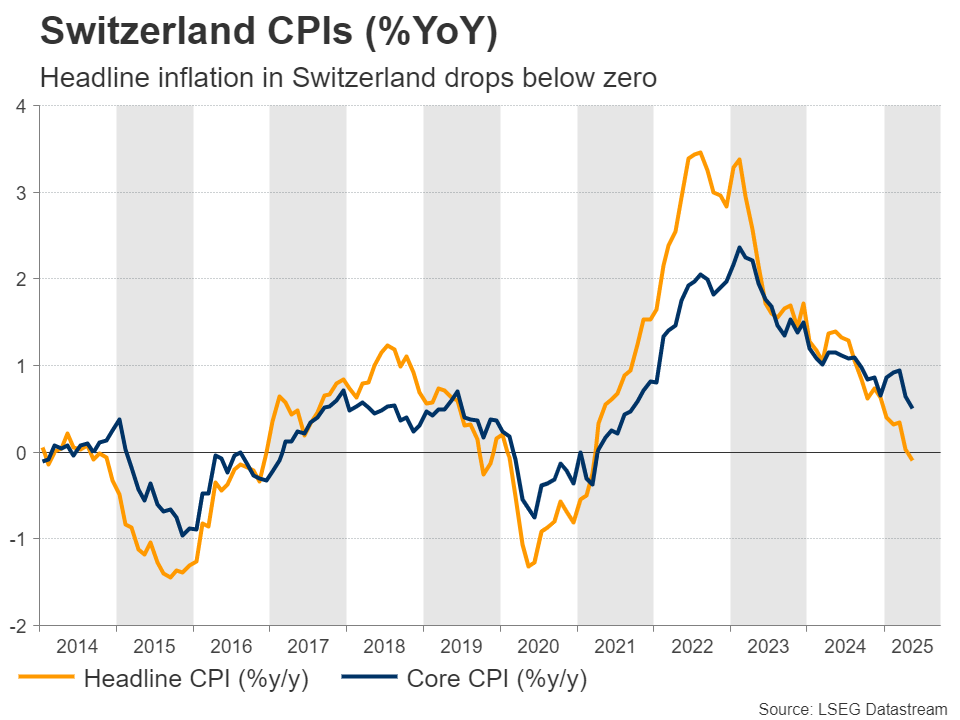

Switzerland’s data for June, due out on Thursday, could also attack special attention. With inflation in Switzerland falling in negative territory, there was speculation that the would cut by 50bps at its prior meeting, taking interest rates into negative territory. This did not happen as the SNB cut by only 25bps to zero.

Now, there is a 30% chance of another rate cut at the September gathering and should Thursday’s data suggest that the nation remained in deflation in June, that probability could go higher, thereby weighing on the , which remains very strong despite the latest wave of risk appetite.