By the time the clock hits 8:30 a.m. in New York today, the Bureau of Labor Statistics will drop July’s — and while it’s just one line of data in the grand market scroll, traders are treating it like the final booby trap before . A new BLS head is waiting in the wings, someone who’s already trashed the status quo, so there’s even a tinge of paranoia that the numbers may be presented with a little less gloss and a little more bite.

The street’s leaning hard — 80.6% probability priced toward a 25bp September . But that’s conditional on one thing: the print doesn’t come in smoking hot. The market’s tolerance band is tight. above 0.40% MoM is hot enough to torch the carefully constructed dove narrative and put a hawkish floor back under the Fed.

The Consensus Script

-

: +0.2% MoM (from +0.3%), Y/Y ticking to 2.8% from 2.7%.

-

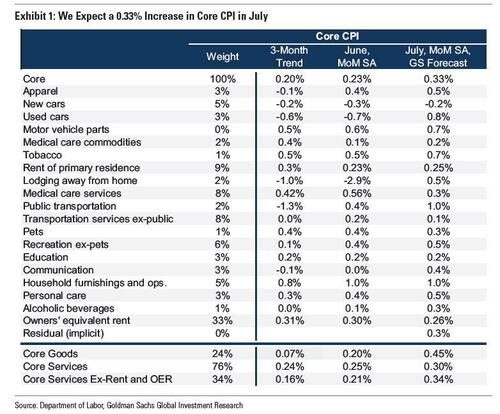

Core CPI: +0.3% MoM (from +0.2%), Y/Y to 3.0% from 2.9%.

-

Forecast distribution is top-heavy — more than twice as many desks see 3.1% as 2.9%.

That skew tells you where the risk is — upside. And in a market that’s been spoon-fed softer prints for four months in a row, an upside break could change the conversation.

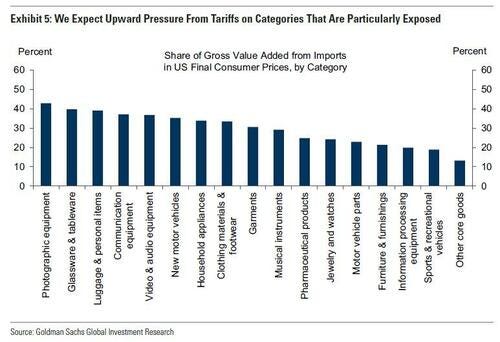

The Tariff Transmission Test

This print is a temperature check on rents and airfares, and the first big read on whether Trump’s latest tariff volleys are finally hitting US consumers. For months, the impact’s been absorbed upstream by foreign producers. Now, the pass-through baton is moving into US store shelves.

-

Core goods are catching a bid: furniture, appliances, electronics.

-

Used cars: Goldman sees +0.75%, driven by auction prices heating up.

-

New cars: -0.2% thanks to fatter dealer incentives.

-

Airfares: +2% as seasonal headwinds battle underlying demand.

-

Household goods & rec/comm gear: +0.12pp from tariffs; autos add +0.02pp.

If that basket delivers, you’re looking at a clean 0.3%–0.4% core print for the next several months. Goldman pegs half of that as tariff-driven noise, the other half as the dying embers of residual inflation. Strip tariffs, and their models take toward 2.5% in 2026 — textbook Fed “mission accomplished.” But with tariffs, the optics get ugly.

The Fed’s Tightrope

The labor market’s wobbling just enough to give the doves confidence: ’s 3-month trend is cooling, steady at 4.2%. Hawks keep hammering that inflation’s above target, but the argument’s losing teeth when the job side of the mandate looks less bulletproof.

-

Kashkari: Would rather cut now and reverse later than sit on his hands — essentially telling markets the Fed’s ready to play offense even without total clarity.

-

Daly: Says the Fed “can’t wait forever” — code for September’s already penciled in.

-

Musalem: “We’re missing on inflation, not jobs” — the line that lets doves keep pressing for easing.

Bottom line: If today’s print is anything shy of “hot-hot,” the cut remains locked. A tariff spike on goods? The Fed can call it transitory. A broad-based surge with services inflation on the boil? That’s where the hawks dig in.

Market Positioning

Complacency is the flavour of the week.

-

: 15.8 — lowest since December.

-

options: pricing a 0.70% absolute move post-print, biggest since May.

-

Street positions: long front-end rates, steepeners, equities, short .

The pain trade is obvious: a hot print smokes all of them at once.

JPM’s CPI reaction grid:

-

Core > 0.40%: SPX –2% to –2.75%.

-

0.35%–0.40%: –0.75% to +0.25%.

-

0.30%–0.35%: flat to +0.75%.

-

0.25%–0.30%: +0.75% to +1.2%.

-

: +1.5% to +2%.

What’s Really at Stake

The September cut is likely coming unless the print is nuclear. However, the CPI print is also about how the Fed frames the move:

-

Is it cutting because inflation’s back under control and tariffs are noise?

-

Or is it cutting with inflation still sticky, admitting growth fears outweigh price risks?

The market narrative shifts depending on that framing. One makes it an “insurance cut” in a still-healthy economy; the other plants seeds for a longer, deeper cutting cycle.

My Trader Read:

-

Core ≥0.4% and services hot → fade SPX, dump steepeners, squeeze likely.

-

Core 0.3%–0.35%, goods-driven → buy the dip in equities, hold steepeners, short USD.

-

Core → risk party continues, VIX sinks, cyclicals and small caps rip.

Today’s number is the gatekeeper to the next Fed pivot. And in a market where traders are acting like volatility’s been deported for the summer, this one print could be the postcard that says it’s coming back.